Weekly Outlook

U.S. Business growth in Services, Low U.S. jobless claims, New Zealand’s and Canada’s labour market growth ahead: All eyes on U.S. CPI data and retail sales

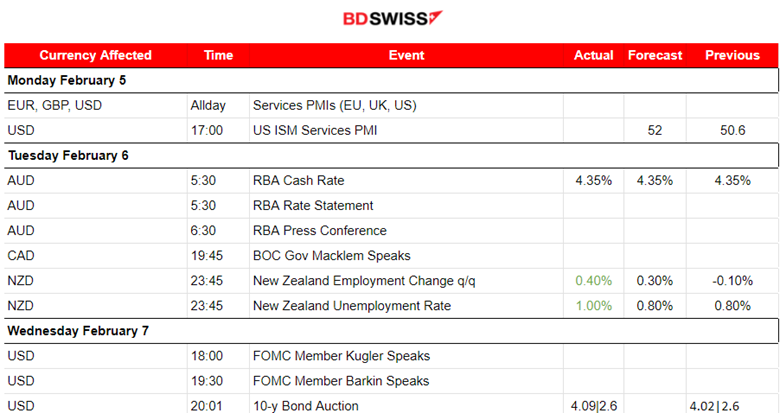

PREVIOUS WEEK’S EVENTS (Week 05-09.02.2024)

Announcements:

U.S. Economy

The U.S. shows significant services sector growth. The PMI increased to 53.4 last month from 50.5 in December. A reading above 50 indicates growth in the services industry, which accounts for more than two-thirds of the economy.

The report suggests that economic growth momentum from the fourth quarter continues, reassuring that cuts in March will not take place. The Federal Reserve left interest rates unchanged last week, but Chair Jerome Powell told reporters that rates had peaked.

New claims for unemployment benefits fell slightly more than expected last week, confirming the views for labour market strength, coinciding with the previous month’s strong NFP data. As long as the labour market remains stable, the economy will continue to grow but inflation is unlikely to continue lowering significantly.

New Zealand Economy

New Zealand’s labour market data showed higher-than-expected employment growth. Employment increased by 0.4%, with the unemployment rate rising to 4.0% in the fourth quarter, below the expectations of a 4.2% unemployment rate.

Canada Economy

Labour market-related reports on Friday showed that Canada added 37K in January, more than double the expected figure, while wage growth slowed slightly and the unemployment rate edged down to 5.7% from 5.8% in December, posting its first decline in 13 months. Its labour market seems resilient. The Bank of Canada (BoC) has kept its key overnight interest rate at a 22-year high of 5% since July, as it strives to bring inflation back to its 2% target. Inflation was 3.4% in December.

______________________________________________________________________

Interest Rates

RBA Rates

The Reserve Bank of Australia (RBA) held interest rates steady as it faces high inflation and stated that further increases are not ruled out. This signals that an easing policy is not coming soon for the RBA. The Board needs to be confident that inflation is moving sustainably towards the target range,” said the RBA Board in a statement.

______________________________________________________________________

Sources:

https://www.reuters.com/world/americas/canada-adds-37300-jobs-january-wage-growth-slows-2024-02-09/

https://www.reuters.com/markets/us/us-service-sector-growth-picks-up-january-ism-survey-2024-02-05/

https://www.reuters.com/markets/new-zealands-jobless-rate-rises-40-fourth-quarter-2024-02-06/

_____________________________________________________________________________________________

Currency Markets Impact – Past Releases (Week 05-09.02.2024)

Server Time / Timezone EEST (UTC+02:00)

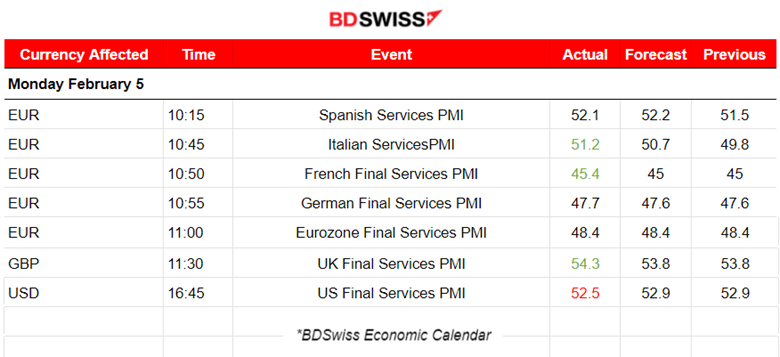

Services PMIs:

Services PMIs:

Eurozone PMIs:

Spanish services remain in expansion, with a PMI figure of 52.1. The growth of the Spanish service sector improved during January amid better market conditions and higher sales. Job growth picked up, accelerating to its best level since May 2023.

In Italy, the PMI shows a turn to the expansion area as it was reported above the 50 threshold, 51.2 from the previous 49.8 points. A sign of recovery across the Italian service sector economy. It experienced improved overall demand conditions and a rise in workforce numbers in January, the third increase in successive months.

The French services sector saw more contraction instead. The downturn extended into January, marking its longest period of contraction in over a decade. Businesses faced generally subdued demand conditions, lower activity and no new business opportunities. However, business confidence ticked up.

The German service sector business activity also contracted for the fourth consecutive month in January. The sector faces an ongoing weakness in demand. Firms improved expectations for activity in the coming year though having a positive impact on labour.

The Eurozone downturn continues, however, at a slower pace. PMI remains at 48.4 points. Contractions in business activity and new orders softened, while growth expectations strengthened to a nine-month high.

United Kingdom PMIs:

The U.K. sees the strongest service sector performance since May 2023. A significant increase in business activity extended the current period of expansion to three months. Higher levels of output, rise in new orders and improved confidence among clients due to strengthening economic conditions and expected interest rate cuts.

United States PMI:

The U.S. business activity continues to grow aggressively. The services PMI reported in the expansion area once more, at 52.5 points. The U.S. services business activity expanded at the fastest pace since June 2023. A quicker rise in new orders, improved demand conditions and an increase in export orders. The U.S. ISM Services PMI is showing expansion at its fastest pace in four months.

_____________________________________________________________________________________________

FOREX MARKETS MONITOR

Dollar Index (US_DX)

The dollar remained on the same level in general last week, after a long volatile path, with volatility levels lowering while approaching the end of the week. From the 6th to the 7th of Feb, the dollar index dropped and found support near 104 points. After consecutively testing that support it did not break it but rather moved to the upside on the 8th rapidly until it found resistance before eventually reversing to the 30-period MA. During that trading day, the dollar gained strength before the unemployment claims data release but after the release (lower Claims) it weakened significantly. With the Fed spreading the commitment to lower rates this year, the dollar index can not stay at high levels. After the 8th Feb the dollar continued to weaken further however, the dollar index remained above the 104 points support.

EURUSD

EURUSD

The pair experience an unusual upward path in general. The ECB stated that talks regarding interest rate cuts are still premature to take place. The EUR is gaining ground against the dollar and it is clear that most of the volatility that the pair experienced while going to the upside is curved by the USD. The drop on the 8th is because of USD appreciation and a following USD depreciation the same day. The pair climbed higher from the USD’s further strong depreciation against other currencies. However, it is important to note that the labour market in the U.S. is showing significant growth which contradicts the views for cuts soon. This probably keeps the dollar stable.

_____________________________________________________________________________________________

_____________________________________________________________________________________________

CRYPTO MARKETS MONITOR

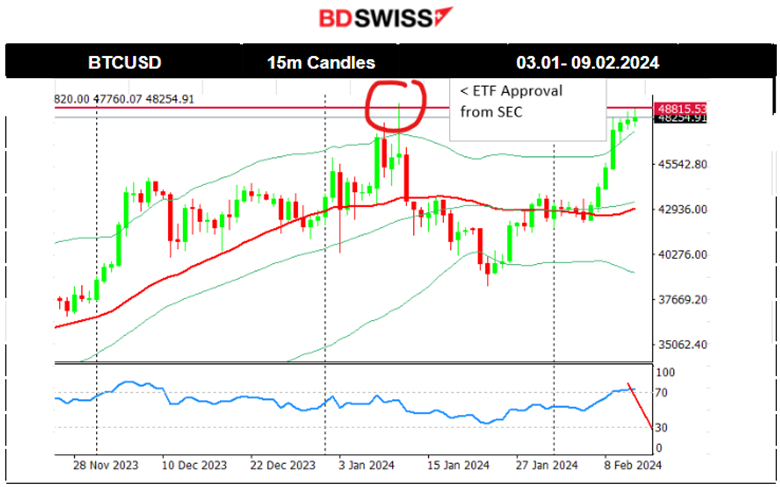

BTCUSD

On the 7th Feb, Bitcoin moved to the upside aggressively. The momentum is quite strong as it seems to break all the Fibo levels, 100 and 161.8 without any significant retracement. Its price continued to the upside aggressively breaking further resistance and eventually reaching the strong resistance at near 48,900 USD, levels last seen during the SEC news regarding the approval of Bitcoin ETFs. Currently, the RSI14 (H1 time frame) shows quite bearish signals for now (lower highs).

____________________________________________________________________________________________

____________________________________________________________________________________________

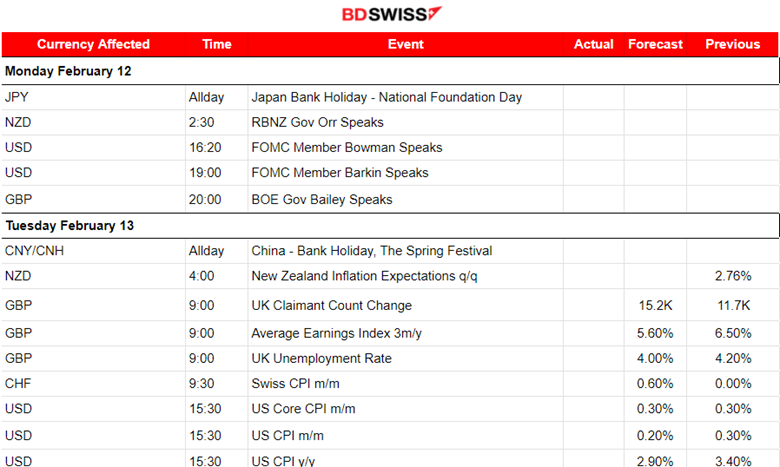

NEXT WEEK’S EVENTS (12 – 16.02.2024)

Coming up:

Big news for the United Kingdom ahead: Inflation, Claimant Count Change, Employment and Average Earnings reports.

The United States Inflation-related data are going to be reported this week (CPI and PPI), figures greatly anticipated by the market and the Central Bank.

Retail Sales reports for both the U.K. and the U.S. are going to be reported as well, giving more information related to the area of spending.

Currency Markets Impact:

_____________________________________________________________________________________________

COMMODITIES MARKETS MONITOR

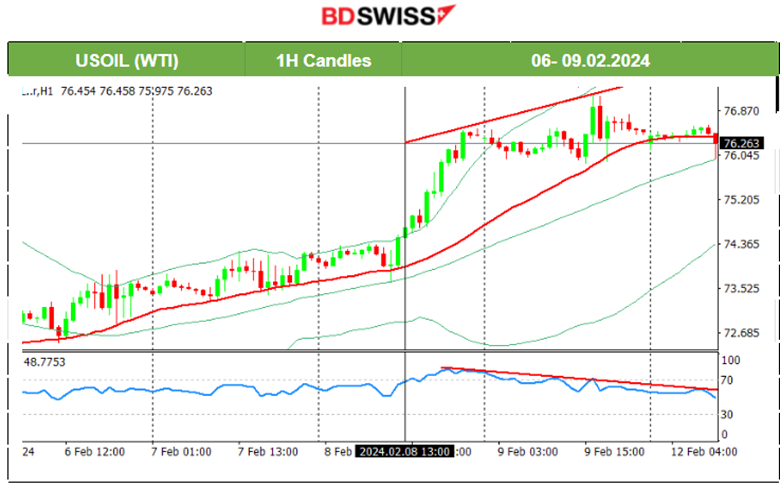

U.S. Crude Oil

Crude’s price reversed from the downtrend following the RSI’s signals of bullish divergence, as mentioned in the previous analysis. After it reached 74.5 USD/b on the 5th Feb, it reversed to the upside, crossing the 30-period MA on the way up and finding resistance at near 73.2 USD/b before retracing. On the 6th Feb, the price moved steadily upwards while being above the 30-period MA. The same happened on the 7th Feb. Surprisingly, crude oil moved significantly higher on the 8th Feb after it broke the apparent channel, as depicted on the chart, reaching the resistance near 76.5 UD/b. On the 9th Feb, the price remained on the same level after a quite volatile trading day. The RSI shows a bearish divergence, indicating that Crude might move significantly lower this week.

Gold (XAUUSD)

Gold (XAUUSD)

On the 8th Feb, Gold broke the upward channel moving to the downside and reaching the support 2020 USD/oz after the USD experienced strong early appreciation. It closed the trading day almost flat since the USD lost strength significantly causing Gold’s price to reverse fully. On the 9th Feb, it experienced another drop testing again that support at near 2020 USD/oz. After an unsuccessful breakout, it eventually retraced to the Fibo 61.8 level.

_____________________________________________________________________________________________

_____________________________________________________________________________________________

EQUITY MARKETS MONITOR

NAS100 (NDX)

Price Movement

On the 6th Feb, the index did not manage to break the resistance at near 17,700 USD and a reversal again followed back to the support at near 17,500 USD. Another reversal sent the index back to the mean. A clear consolidation phase kept the index on the sideways, however experiencing high volatility on the way. On the 7th Feb, the index moved higher breaking the triangle as depicted on the chart and settling near 17,790 USD. On the 8th Feb, the index did not experience strong volatility closing the trading day almost flat, however, on the 9th Feb, it moved to the upside aggressively reaching the area near the 18,000 level. The RSI does not show any signal of the index reversing soon.

______________________________________________________________

Marios Kyriakou

Marios Kyriakou

Recent Posts

Posted on 25 April, 2025 at 12:00 GMT

Posted on 14 April, 2025 at 12:00 GMT

Posted on 26 March, 2025 at 12:00 GMT

Posted on 14 March, 2025 at 12:00 GMT

Posted on 20 February, 2025 at 12:00 GMT